StakeWise DAO has looked at many different $SWISE tokenomics proposals in the past 2 years, but never has the opportunity to make a dramatically positive change felt more tangible than today.

With StakeWise V3 migration on the horizon, we’ve prepared a tokenomics proposal that, in our opinion, ties up the loose ends that stopped some of the previous proposals from going through, and helps StakeWise V3 become a more robust product.

The TL:DR is that we propose to allow $SWISE holders to stake their tokens as collateral for various Vaults in exchange for a share of protocol revenue. In our opinion, StakeWise V3 significantly reduces the risk that a slashing event(s) experienced by one or more node operators will have a negative effect on the $SWISE price, making it suitable for use as an insurance asset.

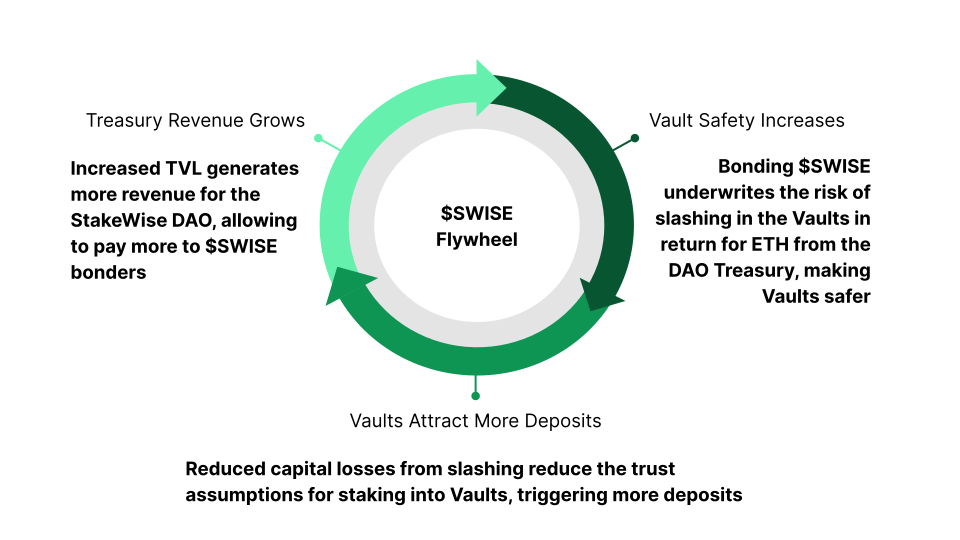

Our goal with this change in the tokenomics is to bring additional safety to StakeWise V3, prompting more deposits into Vaults of all kind, and generating more rewards for insurers over time, kickstarting the flywheel. However, the proposed change is not meant to be definitive - we invite everyone to weigh in and build a strong model from the ground up.

Let’s examine the mechanism in more detail.

Fundamentals

The key innovation of StakeWise V3 is the creation of a staking marketplace that is united by a composable token, osETH. With Vaults expected to carry different perceived slashing risks, stakers are likely to flock to the Vaults that exhibit the most safety qualities & marketing prowess. For example, they could be Vaults run by established staking companies that have the resources and reputation necessary to buy slashing cover, market the Vault to their user base, and grow large enough to establish a network effect.

We’ve seen this story play out before and believe that the StakeWise DAO should limit the extent to which trust (or lack thereof) gives rise to a centralising dynamic in StakeWise V3. We expect solo stakers, who are more than capable of running validators to an enterprise-grade standard, to open Vaults too, and would like to see them receive delegations. The more delegations solo stakers can reach, the greater benefits Ethereum (and stakers) will experience.

With trust the key barrier to receiving delegations, one solution used by DeFi protocols is to require a bond to be posted by solo operators before accepting deposits. We agree with the bonding solution but find that it is not scalable enough. Hence, we see the need for the bond to be placed by external parties. But how should they be compensated, and how much bond should they provide?

As with the open marketplace approach, we believe that the invisible hand should determine both the size of the bond and the premium for it. Pair this with the thirst for a “real yield” narrative and more utility for $SWISE, and we could be onto a winner.

Proposed Mechanics

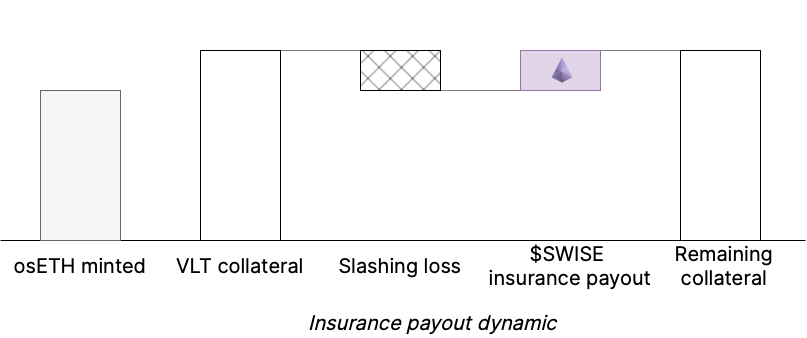

What we are proposing is to allow $SWISE holders to provide bonds to the Vaults of their liking, in form of $SWISE. This means that if the Vault is slashed, the $SWISE provided as a bond would go towards compensating the minters of osETH who incurred losses, capped by the Ether value of the loss.

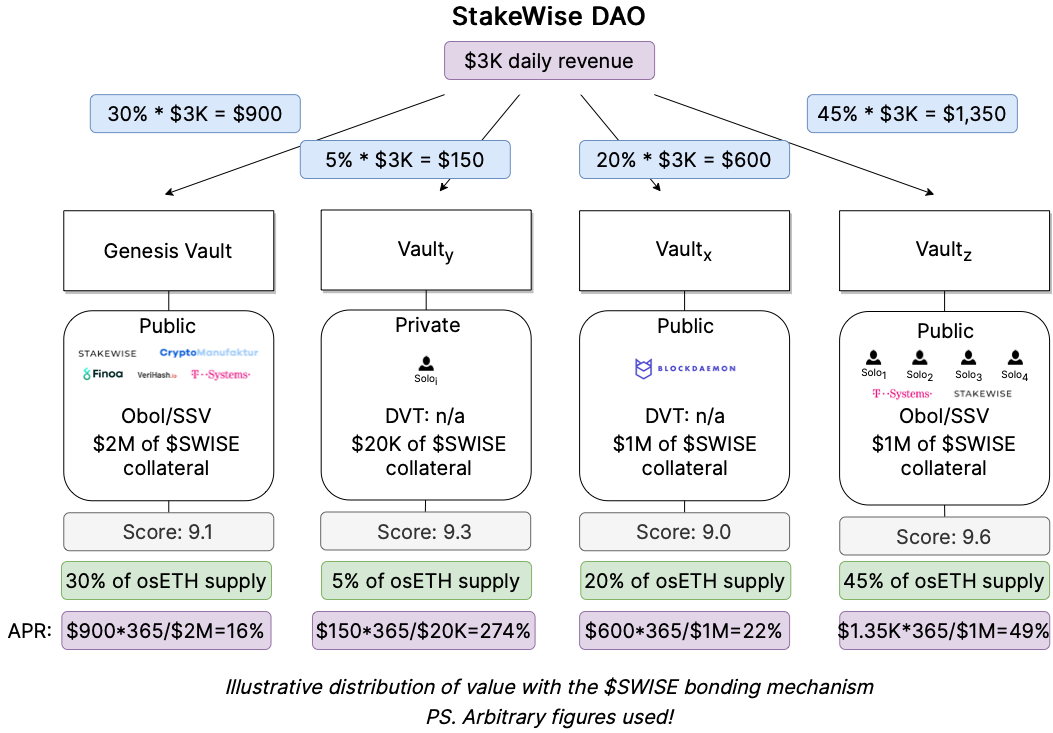

In return, StakeWise DAO would distribute the ETH revenue it accumulates from letting users mint osETH to those who bonded $SWISE. However, there is a caveat - the total value of rewards that can be earned by $SWISE bonders within a particular Vault is capped by the share of osETH that was minted from any given Vault.

For example, if a Vault represents 10% of the total amount of osETH minted in StakeWise V3, then the $SWISE bonders in that Vault are entitled to max 10% of the total revenue distributed by the StakeWise DAO.

With a fixed amount of compensation available, it will be up to the $SWISE holders to assess the merits of providing a $SWISE bond to any given Vault. Their decisions will inform the APR earned from bonding, reflecting the willingness to underwrite the risk of the Vault at the level of compensation they receive.

In the example above, Vault Y has only $20K worth of $SWISE staked as a bond, despite offering a very lucrative revenue share. The annualised yield that results from receiving this revenue is close to 300%. In this case, $SWISE holders looking to bond their $SWISE would need to conduct due diligence into the Vault operator(s) to determine whether such a high APR is a reflection of its high risk, or the lack of attention paid by other bonders to the market conditions. Similar logic applies to other Vaults.

Driven by this competitive dynamic, the equilibrium APR for riskier Vaults will likely settle higher than the APR of the Vaults that are considered less risky. However, the availability of at least some reward in each of the Vaults means that some amount of insurance will likely reach all of the Vaults that have some osETH minted in them, reducing the amount of trust it takes them to attract more delegations. $SWISE bonders will undoubtedly need to conduct extensive due diligence into the Vaults they are planning to underwrite. Yet the beneficiaries of their bonds will likely see an improved Vault Score and a perception of offering more safety, leading to more delegations and the consequent network effect.

Ultimately, V3 is about increasing the ability of Solo stakers to participate in liquid and delegated staking. The $SWISE bonding mechanism will not only help them to get their Vaults off the ground, but also reward the underwriters who believed in them.

Important considerations

As always, the devil is in the details. The finer print on these mechanics would emerge closer to the V3 launch, once the final parameters around osETH, liquidations, and Vaults are agreed upon by the DAO (provided this proposal resonates with the community in the first place). However, there are some rules to the $SWISE bonding mechanism that we already anticipate today:

- Setting a minimal un-bonding period. To stop underwriters from pulling their bonds right when they’re needed, un-bonding should take some time, e.g. 5 days.

- Ensuring $SWISE liquidity remains intact. The $SWISE bonding mechanism incentivizes locking $SWISE away in a contract(s), which could lead to less liquidity being available for low-slippage trading. We could consider requiring to add $SWISE to a Balancer liquidity pool with 90/10 weights between $SWISE and ETH, for example, and then bond using the LP tokens. Keen to hear your thoughts.

- Not all Vaults are created equal, and their “security budget” could differ from the share of osETH they minted if they are more / less risky. We could look to introduce additional considerations for revenue distribution between the Vaults, subject to this making technical and economic sense. Discuss.

Modeling

The team has conducted its own analysis of the potential impact of these mechanics on the $SWISE price & benefits it could offer to stakers, and was satisfied with the results. This is not financial advice - we encourage everyone to conduct their own due diligence (like you would on Vaults) before acting on the proposal.

Discussion

With the StakeWise V3 announcement, the stakes for getting the $SWISE tokenomics right have substantially increased. However, any proposals to introduce changes is preliminary and is not enforced top-down on the DAO members; instead, it is subject to scrutiny and debate.

We invite everyone to analyse the proposal in that spirit. Let us know your thoughts, concerns and opinions, and we’re sure we will get the best tokenomics that StakeWise could land on. LFG ![]()

PS. The figures for $SWISE value, DAO Treasury revenue and APRs used throughout this post are completely illustrative and are not projections or expected values.