Together with Index Coop, StakeWise team brings an idea to launch a $FLI-2xETH/sETH2 liquidity pool, to offer DeFi users a 2x leveraged ETH exposure, staking yield and abundance of trading fees in one place. We call it The Mega Bull Pool, or MBP for short. The DAO’s approval is sought for assigning a portion of $SWISE to the pool to incentivize LPing.

Backstory

For many of us, Ethereum is the core asset in the portfolio. We stake it, lend it, farm with it, and do just about anything to boost the yield. We just can’t get enough of this precious asset - no amount is ever enough. We always look for ways to increase our exposure, and so paycheck after paycheck goes into unbanking ourselves.

Yet what if we could double our exposure without allocating more capital? What if $2,000 worth of ETH bought us $4,000 worth of it? If this were possible, we could earn double without spending double.

Typically, this requires getting into a complicated leveraged position - one must balance factors like collaterization ratio and interest rate in response to changes in the price of a borrowed asset and utilization of a lending pool. These manipulations often require skills beyond those possessed by an average user or are unaffordable due to the gas cost.

Index Coop came up with a great solution to this problem. The creator of the $DPI token recently presented $FLI - a new index that gives users a simple way to get leveraged ETH exposure.

$FLI utilizes Compound Protocol to borrow USDC against ETH as collateral and convert that USDC into more ETH, effectively achieving a 2x leveraged ETH position. To clarify, 2x leverage means that a 10% increase in ETH price results in a 20% gain for the user (same principle applies when the price falls). This is like owning 2x of the ETH you actually hold.

Why would you buy/mint $FLI instead of manually entering into a leveraged position? Easy - holding $FLI only costs 1.95% per year, saves you gas and outsources management of leverage to Index Coop, including during times of market panic. Put simply, it makes boosting your ETH exposure by 2x very accessible.

What’s very important is that the index has an emergency deleveraging mechanism in case of Black Swan events, protecting your capital from liquidation during the downside. The full description of $FLI and its advantages can be found on the Index Coop website.

Before we proceed, here’s an important disclaimer: leveraged products like $FLI always bear a higher risk than vanilla tokens, so you must learn about the risks before using the product.

With that being said, if you understand the risks and are excited about the possibility of higher returns, you will love the ease with which $FLI gives you a bullish exposure to ETH.

Motivation

There are several goals that the StakeWise DAO must achieve to make the protocol successful:

- Maintain a strong peg between ETH and sETH2

- Offer a variety of profitable and safe integrations for sETH2 in the DeFi ecosystem

- Grow the total value locked (TVL) in the StakeWise Pool

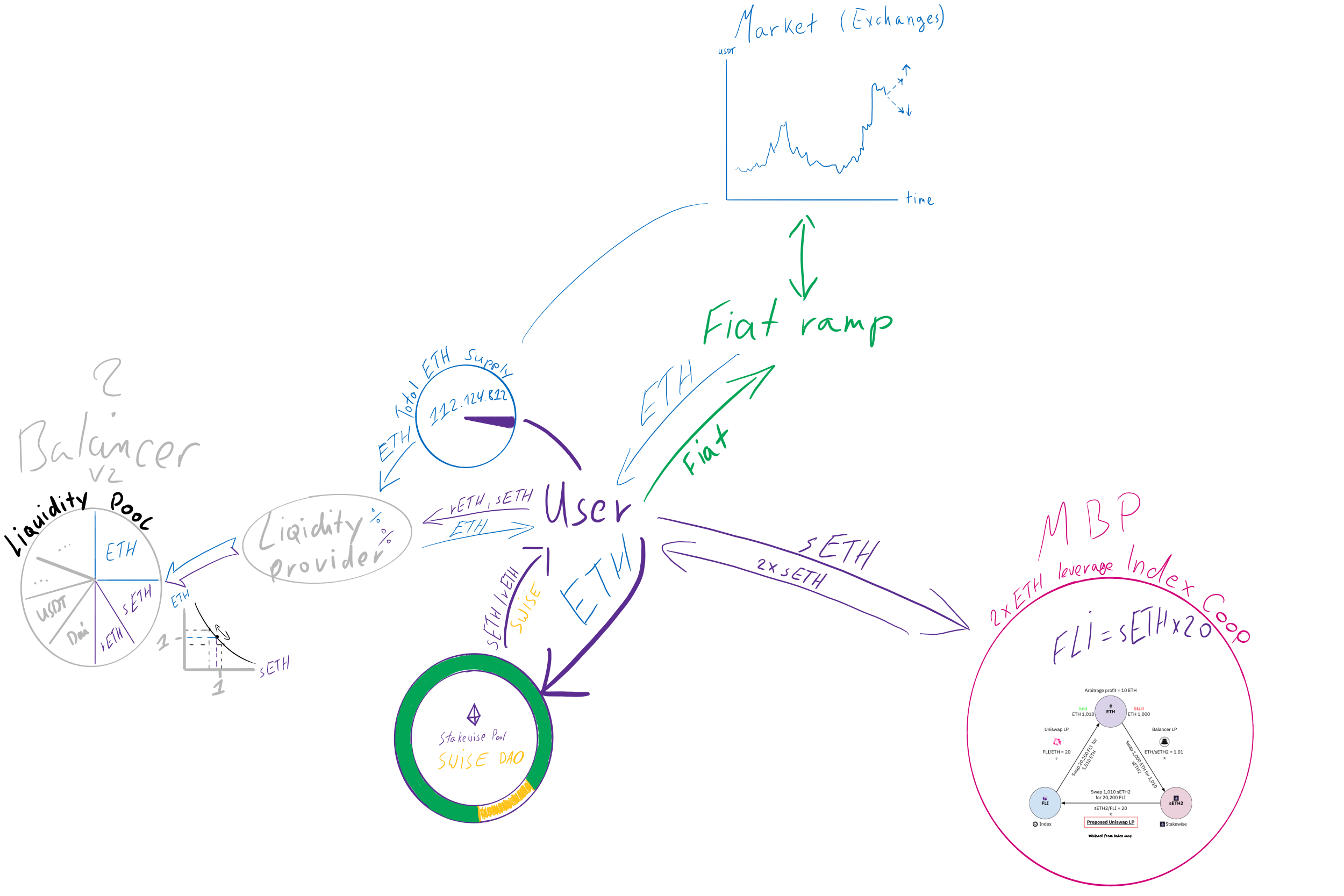

We believe that creating a liquidity pool for the $FLI/sETH2 pair will allow the DAO to check all three boxes. Here’s how.

Maintaining a peg

Chart courtesy of Michael from Index Coop

Alongside achieving ample liquidity for the sETH2/ETH pair with farming incentives, a stronger peg between sETH2 and ETH can be achieved by having arbitrage opportunities in times when the peg is lost. Having an ETH2x-FLI/sETH2 pool alongside an ETH/sETH2 stable pool would give rise to precisely such opportunities, via the following mechanisms (note that $FLI price =/ ETH price because $FLI is an index token):

- Swap (1-x) ETH into 1 sETH2 (where x is the discount) -> swap 1 sETH2 for $FLI -> swap $FLI into 1 ETH = keep the difference between 1 ETH received and (1-x) ETH spent.

Example: assume ETH price is $2,000. Swap 0.98 ETH into 1 sETH2 -> swap 1 sETH2 into 20 $FLI @ $100 a piece -> swap 20 $FLI into 1 ETH = pocket 1 - 0.98 = 0.02 ETH difference. As more volume goes through this arb trade, it will gradually erode the discount, stabilizing the price of sETH2 between the two pools.

- If $FLI/sETH2 is not trading at par, swap (1-x) ETH or $FLI for 1 sETH2 -> swap 1 sETH2 for (1-y) ETH of $FLI (where x and y are the respective discounts in the two liquidity pools), making sure to buy low and sell high to keep the difference between y and x.

Example: assume ETH price is $2,000. Swap 0.97 ETH into 1 sETH2 -> swap 1 sETH2 into 19.6 $FLI @ $100 a piece -> swap 19.6 $FLI into 0.98 ETH = pocket 0.98 - 0.97 = 0.01 ETH difference. As more volume goes through this arb trade, it will gradually erode the discrepancy between the two pools, stabilizing the sETH2 price.

- If ETH price rises y%, swap (1-x) ETH into 1 sETH2 -> swap 1 sETH2 into $FLI @ $Z a piece -> swap $FLI @ $Z+y a piece into 1+y/200 ETH = keep the difference between 1+y/200 ETH received and (1-x) ETH spent.

Example: assume ETH price is initially $2,000 and rises to $2,020 (+1%). Swap 0.98 ETH into 1 sETH2 -> swap 1 sETH2 into 20 $FLI @ $100 a piece -> liquidate 20 $FLI @ $102 a piece into 1.02 ETH = pocket 1.02 - 0.98 = 0.04 ETH difference. As more volume goes through this trade, sETH2 in the ETH/sETH2 pool will be bought up, closing some of the discount, and the price of $FLI between the $FLI/ETH and $FLI/sETH2 pools will stabilize.

In a dynamic market, these arbitrage opportunities will always come up and help sETH2 price discovery, driven by the price fluctuations between ETH, $FLI and sETH2. These opportunities rely on a stable $FLI/ETH peg, which is ensured by the ability to burn and mint $FLI to redeem/spend ETH at par via the Index Coop interface. Also important is that the $FLI holders that are looking to supercharge yields will engage in liquidity provision for the $FLI/sETH2 pool, buying up sETH2 in the process, thus helping to improve the peg.

Offering profitable and safe integrations across DeFi

We expect the ETH2x-FLI/sETH2 liquidity pool to become a high-yielding place to park your assets. There are three sides to this.

- Becoming an LP in the $FLI/sETH2 pool allows to continue earning staking rewards whilst also tremendously benefitting from the rise in ETH price. Unlike the staked ETH tokens of competitors, our dual token model allows to preserve staking rewards when sETH2 is in the liquidity pool, enabling an extra bullish ETH exposure together with passive yield from staking. Another good thing for LPs is the absence of impermanent loss possibility in this pool.

- Availability of multiple arbitrage strategies shall contribute to a high volume of trades in all the liquidity pools involved. For example, in the $FLI/ETH pool alone, the volume of trading reaches a staggering amount (see below). Hence, providing liquidity for this pool would result not only in a bullish ETH exposure with passive staking income, but some high trading fees as well:

24 hrs trading fees in the $FLI/ETH pool work out to 43% APY from trading activity alone

Once DeFi users start exploring the arbitrage opportunities, it would likely result in higher trading fees for the main sETH2/ETH pool as well.

- The pool could be incentivized with both $SWISE and $INDEX tokens to further boost LPs’ yield, pending decisions by the DAOs of respective protocols.

When it comes to safety, there is a strong brand name behind $FLI. Partnering with DeFi Pulse and TokenSets, Index Coop has managed to achieve $136M market cap for its flagship index, $DPI, which offers exposure to a list of the top DeFi projects (DeFi Pulse Index). We have no doubt that $FLI will enjoy a similar success, thanks to its clever mechanisms for automatically keeping leverage between 1.7x-2.3x, frequently re-centering, and utilizing a network of Keeper bots to avoid liquidations in drastic scenarios.

Grow StakeWise TVL

While having a $FLI/sETH2 pool doesn’t directly contribute to a higher TVL, we believe such a pool could boost deposits through the second-order effects like:

- Increased awareness about StakeWise and the advantages of its tokens via existence of the pool and cross-marketing with Index Coop

- Wider market participation in the $SWISE farming mechanisms following initial exposure to the token via liquidity provision in $FLI/sETH2 pool

- Having a stronger peg for the sETH2/ETH pair driven by arbitrage opportunities and deeper liquidity (due to LPs earning more trading fees)

Specification

- A vanilla liquidity pool on Uniswap where $FLI and sETH2 would be initially provided in 50:50 weights. Uniswap is the top choice among DEXs because liquidity there is expected to be the highest. An alternative DEX could be 1inch, where the ability to take/receive overflowing slippage could boost LPs trading fees.

- Both Index Coop and StakeWise teams would propose allocation of $INDEX and $SWISE incentives to LPs of the pool.

- StakeWise and Index Coop would create a separate contract where the rewards from staking (rETH2) and farming (potentially $INDEX, $SWISE) would be collected. LPs would be able to stake LP tokens and collect their fair share of accrued rewards whenever they want.

- In the future, there remains potential to enable usage of LP tokens as money legos in other DeFi protocols.

Risks

We are dealing with leverage, so obviously this product will not be for everyone. Also we might risk fragmenting liquidity for sETH2, although the flows in and out of the main sETH2/ETH pool could be controlled via incentives.

Closing remarks

So here we are: this is an opportunity for the sETH2 holders and the wider market to gain 2x exposure to ETH while earning staking income, trading commissions and whatever farming rewards the two DAOs will agree on. There are hardly any pools out there that come close to this earnings potential, and hence we call it the Mega Bull Pool (MBP).

Please offer your thoughts on this idea and/or suggest other similar assets we could partner with. Viva la StakeWise!

Index Coop’s proposal to their DAO: https://docs.indexcoop.com/products/flexible-leverage-index-fli

at that.

at that. got my vote

got my vote